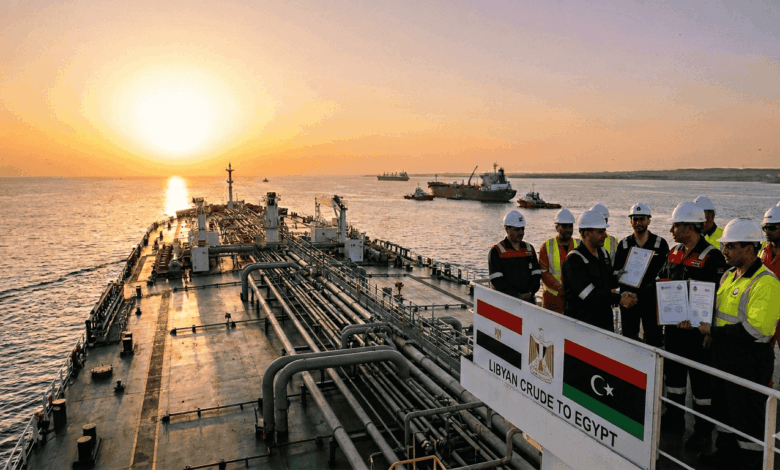

Egypt has begun importing crude cargoes from Libya, with recent flows totaling roughly 1.2 million barrels across two shipments. Each cargo aligns with standard Mediterranean loading sizes of around 600,000 barrels and trades against Brent-linked pricing benchmarks. On the surface, the move reflects routine supply diversification following disruptions in the Gulf due to the current war between Israel, The United States and Iran.

Yet the structure and timing of these shipments suggest a second layer. The emerging trade pattern may also serve as a financial balancing mechanism between the two countries, rather than a simple supply adjustment.

Egypt typically sources crude from a mix of Gulf suppliers, including Kuwait and Iraq, alongside spot cargoes. Recent disruption to Gulf logistics, particularly around key transit routes, forced Cairo to seek alternative barrels that can move through Mediterranean channels with fewer constraints. Libyan crude offers a natural fit. It provides proximity, compatible grades, and established trading routes.

Still, the volumes involved remain modest. Egypt imports an estimated 3.5 to 4 million barrels per month. Libyan cargoes at roughly 1 to 1.2 million barrels per month cover only part of that demand. The shift does not signal a structural pivot in sourcing strategy. It reflects a short-term substitution under logistical pressure.

The more interesting dimension lies in the financial relationship between the two countries. Libya has accumulated significant liabilities tied to electricity imports from Egypt over recent years. These obligations exceeded $400 million at their peak. Authorities moved to settle a large portion of that balance earlier this year, with repayments estimated at around $350 million.

That process leaves an outstanding balance of roughly $140 million.

At current government-linked contract pricing, typically in the range of $85 to $95 per barrel, that remaining liability aligns closely with the value of approximately 1.2 million barrels of crude. The overlap between outstanding debt and current shipment volumes stands out.

This alignment points to a plausible mechanism. Rather than settle the remaining balance entirely in cash, the two sides can offset part of the liability through physical oil deliveries. In practical terms, Libya supplies crude cargoes to Egypt, while both parties account for the value against existing financial obligations.

Such arrangements remain common in state-to-state energy relationships, particularly where foreign currency constraints or payment frictions exist. They allow governments to reduce exposure on both sides of the balance sheet without relying on direct cash transfers. They also provide operational flexibility during periods of market disruption.

For Libya, the structure offers a way to clear outstanding obligations while maintaining export flows. Oil remains the country’s primary revenue source, and redirecting cargoes toward a partner with existing financial ties can streamline settlement. It also reduces pressure on public finances by linking exports to liabilities already on record.

For Egypt, the mechanism provides access to crude without increasing immediate hard currency outflows. The country faces ongoing pressure to manage foreign exchange reserves and external financing needs. Offsetting part of its import bill against receivables from Libya creates space within that constraint.

The pricing framework reinforces the commercial logic. Brent-linked contracts ensure that both sides anchor the transaction to international benchmarks. This reduces disputes over valuation and allows the offset to function within standard market parameters. It also maintains consistency with broader trading practices, even when the underlying settlement includes a financial adjustment.

The structure does not eliminate risk. It depends on continued coordination between institutions on both sides and on the accurate valuation of cargoes against outstanding balances. It also requires transparency to avoid disputes over pricing differentials or delivery terms. Yet the mechanism itself follows a well-established model.

This dynamic adds context to recent headlines. Much of the media narrative has framed Egypt’s move as a strategic shift toward Libyan crude. The data does not support that interpretation. Volumes remain limited, and Egypt continues to rely on a diversified supply base. The current flows address a specific disruption rather than a long-term realignment.

A financial lens offers a more precise explanation. The trade flows align with a narrowing debt balance. They also reflect a broader pattern in regional energy markets, where transactions increasingly combine physical supply with financial settlement.

Periods of geopolitical stress tend to accelerate such arrangements. Disruptions to traditional supply chains force governments to adapt quickly. At the same time, fiscal constraints encourage the use of non-cash settlement tools. Energy trade, with its scale and flexibility, provides a natural channel for that adjustment.

The Egypt–Libya case illustrates this convergence. Supply needs created the immediate opening. Financial alignment shaped the structure of the response. Together, they produced a flow of crude that serves both operational and balance sheet objectives.

Whether the mechanism continues will depend on several factors. A restoration of stable Gulf supply would reduce Egypt’s need for alternative barrels. A full settlement of outstanding liabilities would remove the financial incentive for offset arrangements. Conversely, prolonged disruption or renewed fiscal pressure could extend the current pattern.

For now, the numbers point in a clear direction. Cargo volumes match the scale of remaining debt. Pricing aligns with international benchmarks. The structure fits established models of state-to-state energy settlement.

In that sense, the recent shipments represent more than a stopgap supply measure. They highlight how energy trade can double as a financial tool, particularly in regions where political and economic pressures intersect.